What higher borrowing costs mean for loans, savings, and household budgets in 2026

Rising interest rates are no longer just a concern for economists or financial markets. In 2026, they are directly influencing how ordinary consumers spend, save, borrow, and plan for the future. From higher loan payments to shifting job markets and tighter household budgets, elevated interest rates are quietly reshaping daily life across the globe.

As central banks keep rates higher for longer to combat inflation, consumers are feeling the ripple effects in nearly every aspect of their financial lives.

Why Interest Rates Are Staying High

Interest rates have climbed sharply since the post-pandemic economic recovery, driven by persistent inflation, supply chain disruptions, geopolitical tensions, and rising government debt. Central banks—including the U.S. Federal Reserve, the European Central Bank, and others—have signaled caution about cutting rates too soon, fearing a resurgence of inflation.

This prolonged high-rate environment means borrowing remains expensive, while savings yield higher returns—but not without trade-offs.

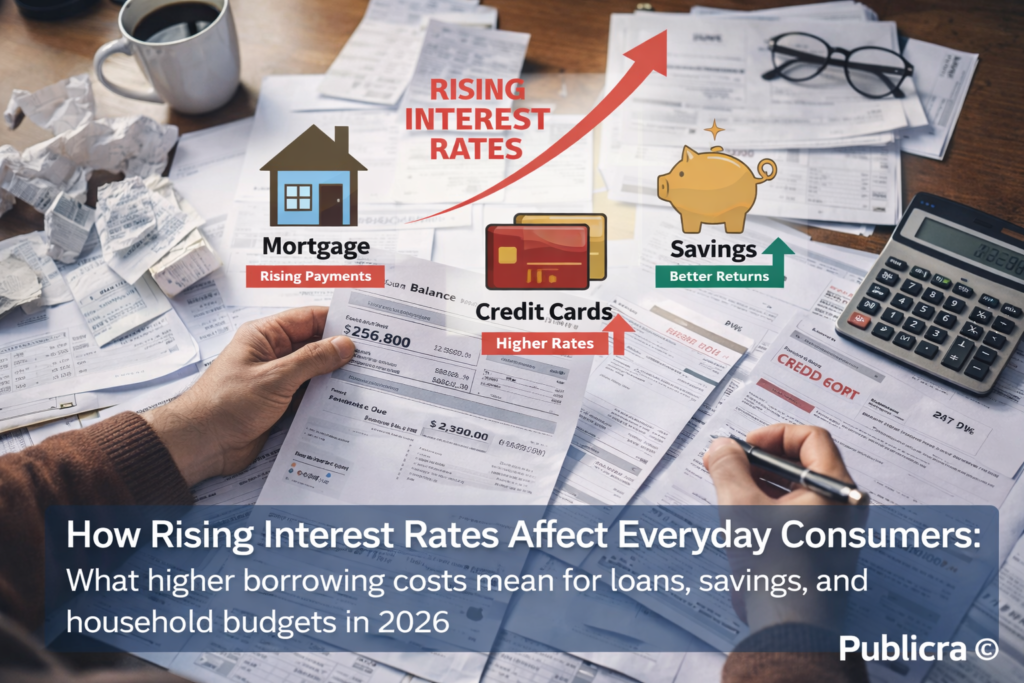

Higher Loan Costs Hit Household Budgets

One of the most immediate effects of rising interest rates is the increased cost of borrowing.

Mortgages and Housing

Homebuyers face higher monthly mortgage payments, making homeownership less affordable for first-time buyers. Adjustable-rate mortgages have become especially costly, forcing some households to delay buying or downsize their housing plans.

Renters are also affected, as landlords pass higher financing costs onto tenants through increased rents.

Car Loans and Personal Credit

Auto loans now come with higher interest charges, raising the total cost of vehicle ownership. Consumers relying on personal loans or installment plans are paying more over time, even for everyday purchases.

Credit Card Debt Becomes More Dangerous

Credit card interest rates typically rise alongside central bank rates, often exceeding 20 percent annually. For consumers carrying balances, this means debt grows faster, making it harder to pay down.

As a result:

- Minimum payments increase

- More income goes toward interest instead of essentials

- Financial stress rises, particularly among middle- and lower-income households

Savings Accounts and Fixed Deposits Finally Pay More

While borrowing has become more expensive, savers are seeing some benefits. Banks are offering higher interest on savings accounts, fixed deposits, and money market funds.

For cautious consumers, this environment encourages:

- Emergency fund building

- Reduced discretionary spending

- A shift away from risky investments

However, inflation still erodes purchasing power, meaning higher interest earnings do not always translate into real financial gains.

Impact on Jobs, Wages, and Spending

Higher interest rates tend to slow economic activity. Businesses face higher borrowing costs, which can lead to:

- Delayed hiring

- Slower wage growth

- Reduced expansion plans

Consumers may notice fewer job openings, tighter salary negotiations, and cautious corporate spending—factors that indirectly influence household confidence and spending habits.

Everyday Prices and Lifestyle Adjustments

Although interest rates aim to curb inflation, price pressures remain uneven. Essentials like food, healthcare, education, and insurance continue to strain budgets.

To cope, many consumers are:

- Cutting non-essential subscriptions

- Postponing large purchases

- Comparing prices more aggressively

- Increasing reliance on budgeting apps and financial planning tools

Long-Term Financial Planning Becomes More Important

Rising rates have renewed focus on financial discipline. Consumers are reassessing:

- Debt repayment strategies

- Fixed vs. variable interest loans

- Retirement savings allocations

Financial advisors increasingly recommend reducing high-interest debt first, locking in fixed-rate loans where possible, and maintaining liquidity amid uncertainty.

What Consumers Can Expect Next

Most economists expect interest rates to remain elevated through much of 2026, with gradual easing only if inflation cools sustainably. For consumers, this means continued pressure—but also opportunities to strengthen financial resilience.

Understanding how interest rates affect everyday decisions can help households adapt, plan smarter, and weather ongoing economic uncertainty.